Market Insight | Space Data Without Buyers: Why Commercial EO Is Struggling to Convert Insight Into Revenue?

The commercial EO market has solved sensing, now it must solve selling...

Why is Earth Observation (EO) adoption lagging despite unprecedented data availability?

For more than a decade, the Earth Observation sector has repeated a familiar promise: more satellites, more data, more insight, more value. On the supply side, that promise has largely been delivered. Constellations have multiplied, revisit rates have collapsed from days to minutes, and analytics pipelines powered by AI now extract patterns that once required entire intelligence units.

Yet commercially, the sector is underperforming.

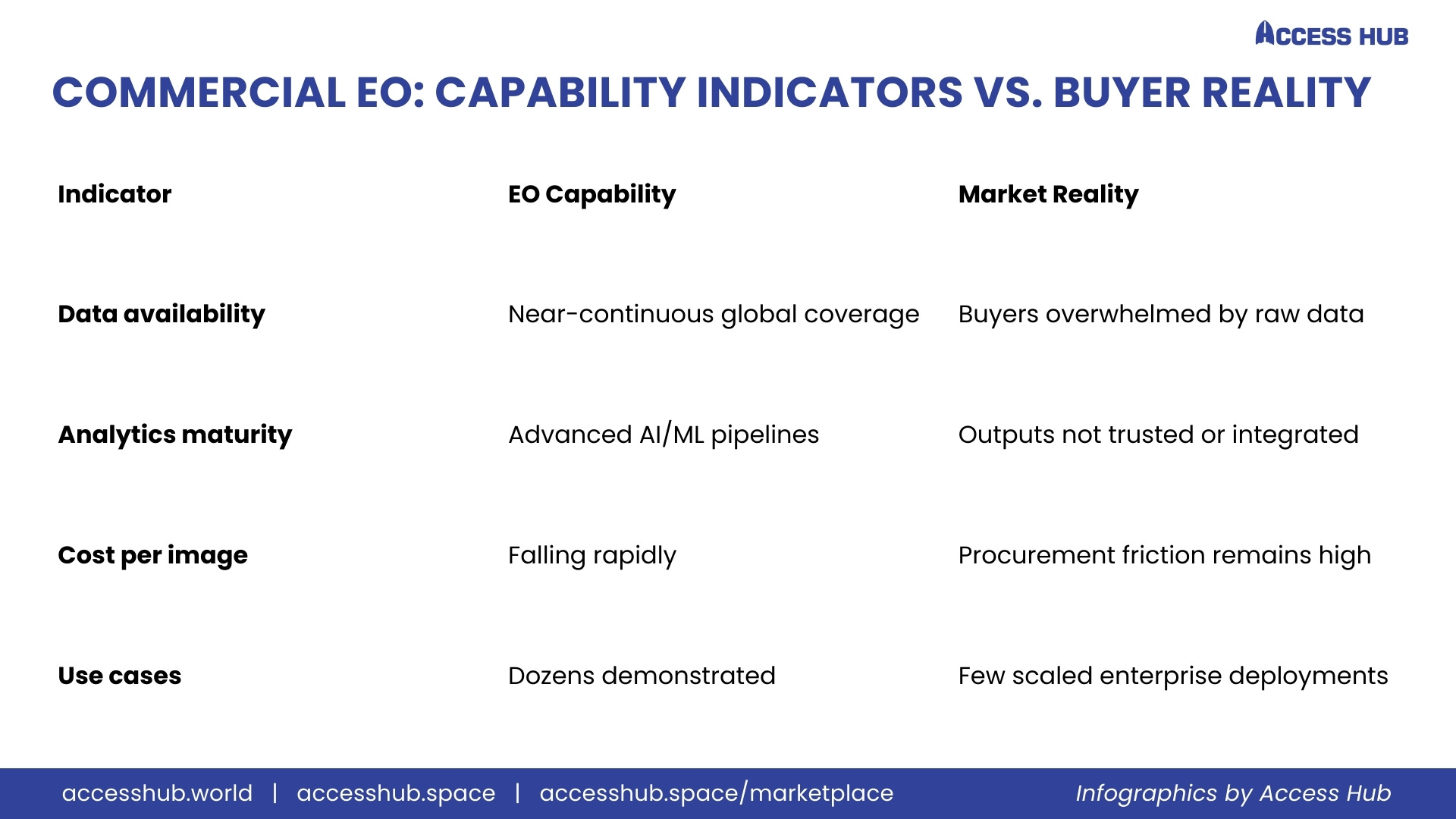

Despite billions invested into EO startups and constellations, most companies remain trapped in pilot projects, low-value data contracts, or public-sector dependency. Outside a narrow set of defense and intelligence buyers, EO adoption remains stubbornly slow. Revenue growth lags capability growth. Insight exists, but buyers do not scale.

This is not a data problem. It is a market design problem.

From my vantage point, working across defense, space, and government stakeholders, the commercial EO sector is not failing because its technology is immature, but because it has misunderstood how decisions are actually made inside its target markets.

The EO Paradox: Abundance Without Adoption

Today’s EO ecosystem is defined by abundance. Companies such as Planet Labs, Vantor, and Airbus Defence and Space deliver global, persistent imagery at resolutions that were once classified. Synthetic Aperture Radar (SAR) players like ICEYE and Capella Space can see through clouds, darkness, and smoke.

On paper, EO should be indispensable.

Governments face climate volatility, infrastructure stress, border instability, and resource scarcity. Defense agencies require persistent situational awareness. Insurers need risk visibility. Energy and mining companies operate in remote, contested environments.

Yet EO adoption remains narrow.

The Reality Check

The problem is not whether EO can generate insight. The problem is whether EO outputs align with decision authority, timing, and accountability inside customer organizations.

The Government EO Trap: Data Moves Faster Than Bureaucracy

Most commercial EO companies still rely heavily on governments as anchor customers. This dependence is understandable. Agencies like the U.S. National Reconnaissance Office (NRO), the European Space Agency (ESA), the National Aeronautics and Space Administration (NASA), and ISRO have budgets, technical literacy, and long-term demand.

But this reliance has distorted EO product design.

Decision Cycles Do Not Match Data Cycles

Government decisions, especially outside intelligence, move slowly. Budget approvals, inter-agency coordination, and political oversight often operate on annual or multi-year cycles. EO companies, meanwhile, pitch real-time insights, daily monitoring, and continuous updates.

This mismatch is fatal.

An EO platform that delivers weekly infrastructure degradation alerts is useless if the responsible ministry reviews assets once per quarter. Flood-risk analytics mean little if disaster funding is allocated after the event.

EO companies confuse technical timeliness with institutional relevance.

Case in Point: Climate and Environment

Programs such as Copernicus under the European Commission generate world-class environmental data. Yet downstream commercial adoption remains limited. Ministries often use EO for reporting, not for operational decision-making. Commercial vendors hoping to sell “decision intelligence” instead encounter reporting workflows optimized for compliance, not action.

Defense Adoption: High Interest, Narrow Doors

Defense is often cited as the EO sector’s strongest growth market. There is truth here, but also a misconception.

Agencies like the U.S. Department of War, NATO, and the UK Ministry of Defence increasingly recognize the value of commercial space. Programs such as the Commercial Augmentation Space Reserve (CASR) signal intent to integrate private capabilities.

But EO vendors underestimate how conservative defense procurement actually is.

EO Is Rarely the Decision Driver

In defense, EO is one input among many: signals intelligence, human intelligence, cyber intelligence, and operational reporting. Imagery, even with analytics, rarely triggers decisions on its own. Commanders require fused, validated, and contextualized intelligence.

EO companies that market “actionable insight” without embedding into existing command-and-control systems face rejection, not because the data is poor, but because it disrupts established chains of responsibility.

Integration Beats Innovation

Defense buyers do not want dashboards. They want EO data integrated into platforms operated by primes such as Lockheed Martin, Northrop Grumman, Raytheon, and Thales.

For EO startups, this means one thing: selling analytics is less important than selling interoperability.

Commercial Markets: EO as a “Nice to Have”

Outside government and defense, EO faces a different challenge: weak decision ownership.

Infrastructure and Utilities

Infrastructure operators acknowledge EO’s value for asset monitoring, but responsibility is fragmented. Engineering teams want data. Finance teams control budgets. Risk teams worry about liability. EO rarely sits clearly within any one cost center.

Without a single accountable buyer, EO deployments stall at proof-of-concept.

Insurance and Finance

Firms like Munich Re and Swiss Re actively explore EO for risk modeling. Yet EO rarely replaces existing actuarial models; it supplements them. As a result, EO budgets remain small relative to perceived strategic importance.

Energy and Resources

Oil, gas, and mining companies increasingly use EO, but often through service providers such as Schlumberger or Wood Mackenzie. EO vendors rarely own the customer relationship.

Why Analytics, Not Imagery, Will Define Winners

The commercial EO market’s next phase will not be won by higher resolution or faster revisit. It will be won by analytics aligned with decisions, incentives, and risk transfer.

Imagery Is a Commodity

High-resolution imagery is now widely available. Competition drives prices down. Differentiation based on pixels is unsustainable.

Analytics Must Answer “So What?”

Successful EO companies will move from describing the world to quantifying consequences:

How much financial risk does this infrastructure defect create?

What operational decision should change as a result?

Who is accountable if the insight is wrong?

This requires domain expertise, not just AI.

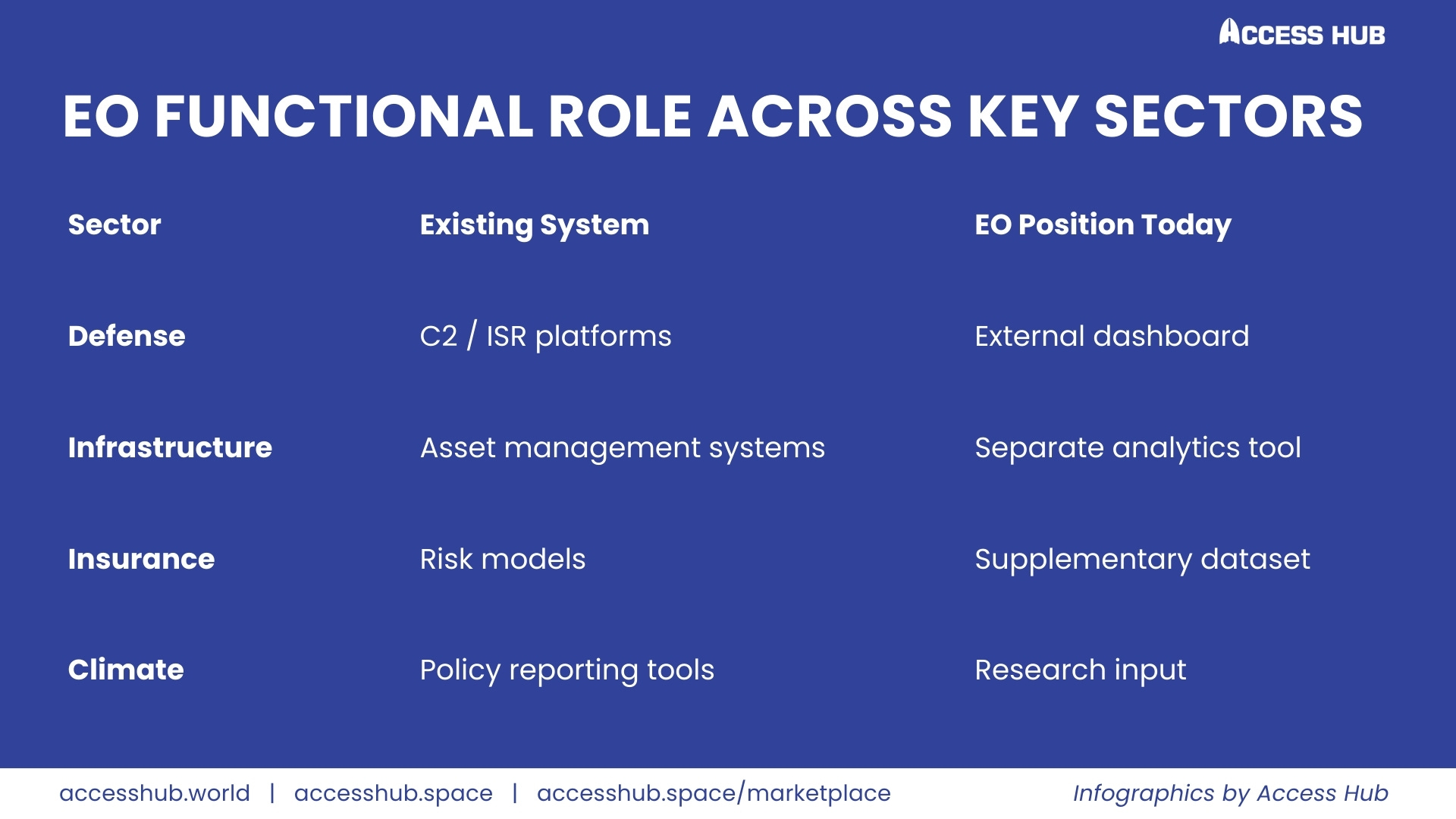

The Integration Gap: EO Outside the Stack

One of EO’s biggest commercial failures is its isolation from enterprise systems.

Where EO Should Live - but Doesn’t

Until EO outputs flow directly into the systems where decisions are executed, adoption will remain limited.

Who Actually Wins in the Next EO Cycle?

The next winners in EO will not look like traditional space companies.

They will be:

Analytics-first, not satellite-first

Embedded into customer workflows

Willing to sacrifice imagery margins for long-term integration

Comfortable selling through primes and integrators

Likely Market Outcomes

A Strategic Reset for EO Startups

For EO startups and analytics providers, the path forward requires uncomfortable shifts:

Design for procurement reality, not technical elegance

Sell fewer dashboards, more embedded decisions

Partner with primes instead of competing with them

Price for outcomes, not data volume

Most importantly, EO companies must stop asking, “What can our data do?” and start asking, “Who is empowered to act on this?”

Until that question is answered, EO will remain rich in insight and poor in revenue.

Conclusion: EO’s Commercial Reckoning

Earth Observation is no longer a technology in search of validation. It is a market in search of alignment.

The satellites are in orbit. The data is flowing. The analytics work.

What is missing is not capability, but commercial empathy.

EO will scale when it learns to think like its customers, speak their institutional language, and integrate into their decision structures. Those who do will define the next decade of the space economy. Those who don’t will continue to marvel at their own data, while wondering why buyers never show up.

Today’s defense and space markets reward those who act on intelligence, not just collect it. That’s where Access Hub steps in.

We go beyond headlines to decode market movements, connect innovators with decision-makers, and help organizations convert strategic insight into real business traction across Space, Defense, Aerospace, Maritime, Media-Tech, and Energy Markets.

If your team is navigating these fast-moving domains, Access Hub is your partner for clarity, connection, and competitive edge. Contact us at: www.accesshub.world